Yuri Gripas/Reuters

- The Treasury market is defying Fed messaging and signs of lasting economic damage.

- Soaring yields signal investors expect the Fed to lift interest rates well before past estimates.

- Fed officials will likely need to address the bond-market rout to avoid disruption to the economic recovery.

- Visit the Business section of Insider for more stories.

The Treasury market has made it clear: the Federal Reserve is a downer.

Optimism toward the US economic recovery flourished over the past week. Daily COVID-19 case counts fell further from their January peak. Vaccinations continued across the country, hinting the pandemic could fade in just a few months. Economic data beat expectations. And Democrats pushed forward with President Joe Biden’s $1.9 trillion stimulus proposal, aiming to accelerate the rebound even more.

And yet, these encouraging developments fueled a sudden shock in the Treasury market.

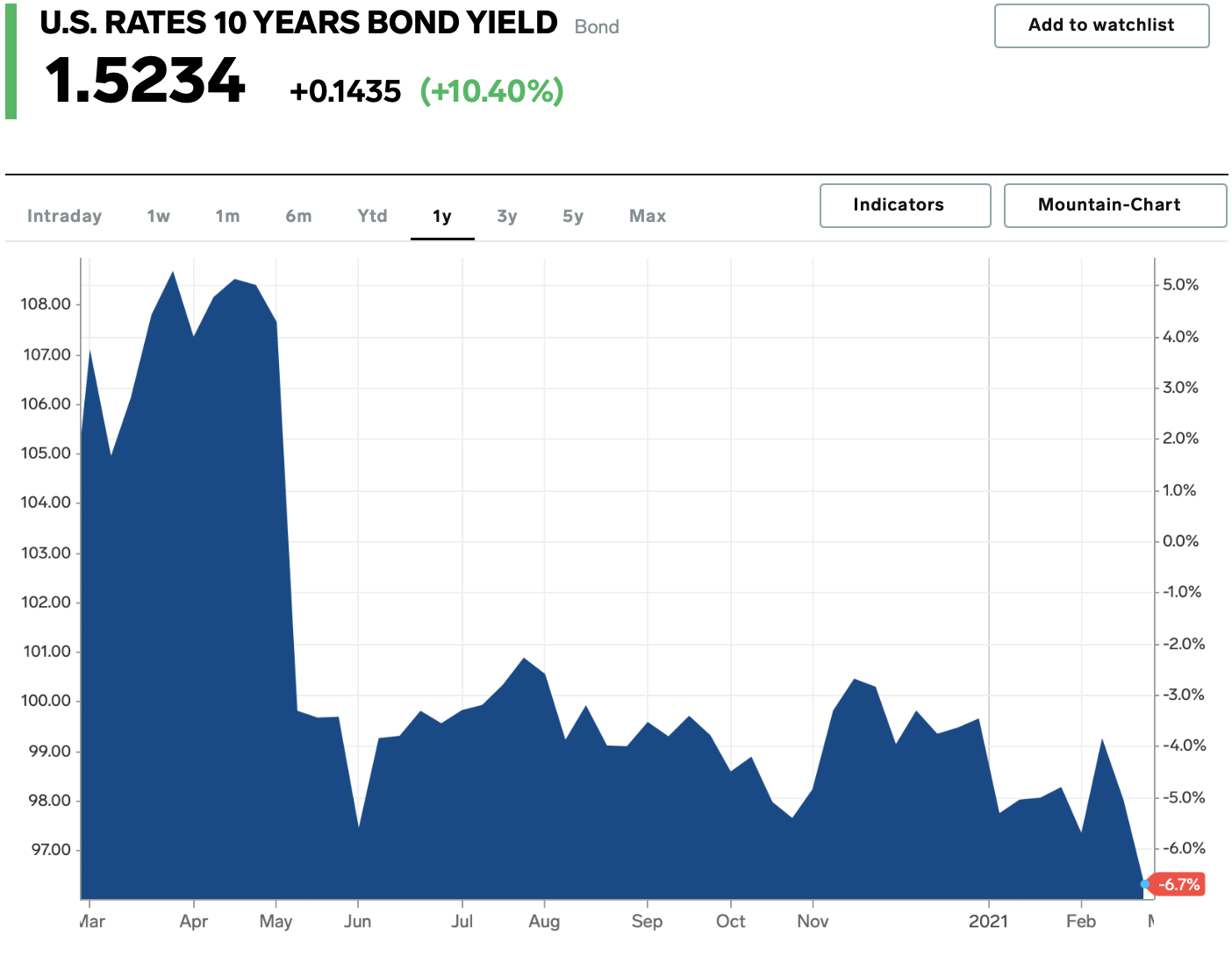

Investors looking to capitalize on a swift recovery dumped government bonds and pushed cash into riskier assets. The 10-year yield soared as high as 1.614% on Thursday, its highest level since the pandemic first slammed the US. The jump immediately cut into stocks’ appeal and dragged major indexes lower throughout the week.

The narrative behind the move is simple: The increased likelihood of new stimulus juicing the recovery lifted expectations for faster economic growth and inflation. Stronger price growth leads investors to demand higher yields.

Yet the market moved to such an extreme that it now stands in contrast with the Federal Reserve's own forecast. The central bank has indicated it doesn't expect inflation to reach its above-2% target until after 2023. The outlook suggests the Fed will hold interest rates near zero through 2023.

The sell-off in Treasurys, however, signals investors are pricing in a rate hike as early as the second half of 2022.

"We're now getting to the point where the market isn't necessarily believing what the Fed is telling," Seema Shah, chief strategist at Principal Global Investors, told Insider. "We've now moved to a slightly more concerning ground, where it seems like the Fed's messaging is not powerful enough."

Too much of a good thing

Central bank policymakers have so far held their ground. The jump in yields suggests investors are expecting a "robust and ultimately complete recovery," Fed Chair Jerome Powell said Tuesday. The chair reiterated that the Fed won't cut down on asset purchases or consider rate hikes until it sees "substantial further progress" toward its inflation and employment targets.

At its core, the sell-off is merely part of the reflation trade, a strategy used to profit from stronger price growth. But the pace at which yields rose is cause for concern, Kathy Bostjancic, head US financial market economist at Oxford Economics, said.

Thursday's leap was the biggest single-day move since December, and overall bond-market volatility rocketed to its highest since April, according to Bloomberg data. Finally, the gains came despite the Fed continuing to buy at least $80 billion in Treasurys each month.

Bank of America Global Research

Since yields serve as the benchmark for the global credit market, a sudden rise can rapidly lift borrowing costs, sending rates for mortgages, car loans, and even utilities higher.

If yields gain too much, too quickly, the price action can be "destabilizing," Bostjancic said. The shock would come as real unemployment still stands at around 10% and industries hit hardest by the pandemic remain far from full recoveries.

"It could choke off this nascent recovery before it gets going," she said.

Others aren't so concerned. Bank of America strategists led by Gonzalo Asis said the trend was less inspired by rate-hike expectations and simply a case of "buying the fundamental dip" before strong economic growth.

There's room for yields to climb higher still, Bostjancic said. Real yields - nominal yields adjusted for inflation - remain negative, signaling there's still enough weakness in the economy to warrant parking cash in the safe haven.

Looking back to look ahead

To be sure, this is far from the first time markets have abruptly reacted to tightening fears.

Concerns of premature tightening of monetary policy fueled the now-famous "taper tantrum" of 2013, when investors rapidly dumped Treasurys after the central bank announced it would reduce the pace of its asset purchases, fueling a sudden - albeit temporary - shock to the bond market.

The Fed will likely move first in this case to avoid additional Treasury-market drama, Bank of America economists led by Michelle Meyer said in a Friday note. Updated economic forecasts set to be published after the Federal Open Market Committee's mid-March meeting should offer some hints at when the Fed's rate-hike criteria could be reached, the team said.

"The risk, however, is that the Fed won't have the luxury of waiting for the next meeting and will have to respond to the abrupt market moves in speeches this week," the economists added.

If the taper tantrum is anything to go by, communication is a difficult balancing act for the central bank. Powell has already said he doesn't expect any stimulus-fueled jump in inflation to be "large or persistent," but that commentary did little to calm the sell-off in Treasurys.

Unless the Fed further clarifies its inflation target, investors will remain in the dark as to when tapering could arrive, Shah said.

"There's so much room for interpretation in terms of how long inflation has to be above 2%, at what level does inflation need to be above 2%," she said. "That lack of clarity gives the market that room to wonder, 'what does the Fed actually mean by that?'"